You fill your prescription for a generic drug-something you’ve taken for years-and the pharmacist says it’s $45 instead of your usual $5. You’re confused. It’s the same medicine, right? Same active ingredient. Same pill. Same doctor’s order. So why the huge jump?

It’s not about the drug. It’s about the contract.

Most people assume that all generic drugs are treated the same by insurance. They’re not. Your plan uses something called a tiered formulary, a system that sorts medications into levels based on cost, not clinical value. Tier 1 is usually the cheapest-often $0 to $15 for a 30-day supply. That’s where most generics live. But not all of them. Some generics, even ones that are chemically identical to the Tier 1 version, end up in Tier 2 or even Tier 3. Why? Because the company that makes that particular generic didn’t pay enough of a rebate to the Pharmacy Benefit Manager (PBM). It’s not about safety. It’s not about effectiveness. It’s a business deal. PBMs like CVS Caremark, Express Scripts, and OptumRx negotiate discounts with drug manufacturers. The bigger the discount, the lower the tier. If a generic drug maker offers a better deal, their version gets placed in Tier 1. The others? They get bumped up. Even if they’re the exact same pill.How tiered copays actually work

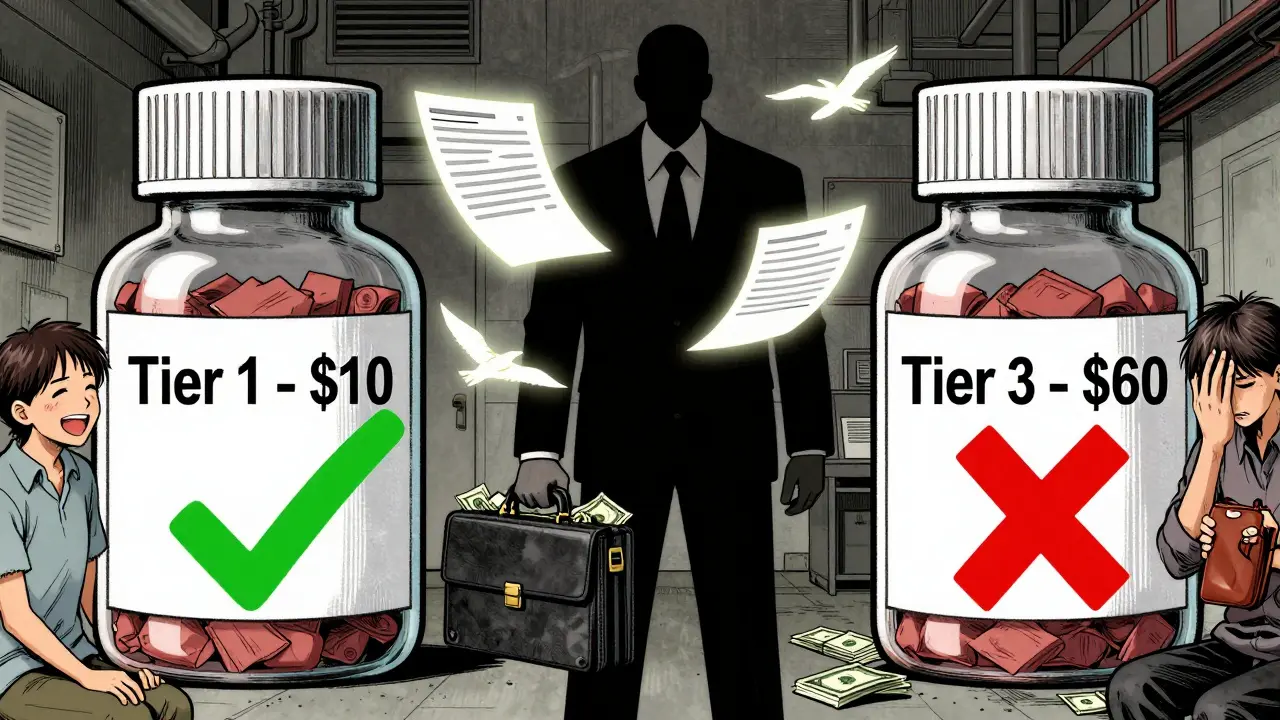

Most plans have four or five tiers:- Tier 1: Preferred generics. Usually $0-$15.

- Tier 2: Preferred brand-name drugs. Around $25-$50.

- Tier 3: Non-preferred brand-name drugs. $60-$100.

- Tier 4: Preferred specialty drugs. 20-25% coinsurance.

- Tier 5: Non-preferred specialty drugs. 30-40% coinsurance.

Why your insurance doesn’t care if it’s the same pill

Imagine you have two brands of aspirin. One costs $2. The other costs $3. They’re both 325 mg, made by different companies. Your insurance picks the $2 one as preferred because the manufacturer gave them a bigger cut. The $3 version? Still fine. Still safe. Still effective. But now you pay more. That’s what’s happening with your prescription. Your plan doesn’t care which generic you take. They only care which one gave them the biggest discount. And if your doctor prescribed a version that doesn’t have that deal, you’re stuck paying the difference. This isn’t rare. In 2023, 41% of insured patients ran into a situation where a generic drug cost more than they expected. And 68% said their insurer gave them no clear reason why.

What you can do when your generic gets bumped

You’re not powerless. Here’s what works:- Check your formulary. Every plan updates it once a year, usually in October. Log into your insurer’s website and search for your drug. See what tier it’s on.

- Ask your pharmacist. They know which generics are preferred. If you get a different version, ask: “Is there another generic that’s cheaper?” Often, they can swap it without calling your doctor.

- Request a therapeutic interchange. This is a form your doctor can fill out asking the insurer to cover the non-preferred drug because it’s medically necessary. It works 63% of the time.

- Use GoodRx or SmithRx. These tools show you cash prices and which tier your drug is on. Sometimes, paying cash is cheaper than your copay.

- Appeal. If your drug was moved to a higher tier mid-year, you can file an exception. You have 72 hours for urgent cases. Write a note from your doctor explaining why switching hurts your health.

The bigger problem: specialty generics

Some of the worst surprises come with drugs for chronic conditions. Take adalimumab (Humira). The generic version came out in 2023. But instead of being a cheap Tier 1 drug, it’s in Tier 4 or 5. Why? Because it’s expensive to produce. Even though it’s a generic, you might pay 30% coinsurance on a $7,000 monthly dose. That’s $2,100 out of pocket. That’s not an outlier. In 2023, 12-18% of generics were classified as specialty drugs. Many patients with autoimmune diseases are shocked when their monthly bill jumps from $30 to $2,000 overnight. And they’re told, “It’s just a generic.”

Why the system won’t change soon

Tiered copays exist because they save insurers money. Studies show they reduce drug spending by 8-12%. That’s why 98% of employer plans and 99% of Medicare Part D plans use them. But the system is broken for patients. It rewards financial deals over clinical sense. And it creates confusion. A 2022 study found that when a drug moved from Tier 2 to Tier 3, adherence dropped by 7.3%. People stopped taking their meds because they couldn’t afford it-even though the drug hadn’t changed. The Inflation Reduction Act, starting in 2025, will cap out-of-pocket drug costs at $2,000 a year. That’s a win. But it won’t fix tiering. You’ll still pay more for the same drug just because your insurer didn’t get a good deal.What to remember

Your generic isn’t expensive because it’s bad. It’s expensive because the manufacturer didn’t pay enough to the middleman. And you’re the one who pays the difference. Next time your copay jumps, don’t assume it’s a mistake. Check your plan’s formulary. Talk to your pharmacist. Ask your doctor to help you switch to a preferred version. And don’t let silence from your insurer stop you from fighting back. The system isn’t designed to make sense. But you can still make it work for you.Why is my generic drug more expensive than the brand-name one?

It’s not common, but it happens. Some brand-name drugs are placed in lower tiers because the manufacturer pays a large rebate to the PBM. Meanwhile, a generic version with no rebate ends up in a higher tier. The brand may cost $100, but your copay is $50. The generic costs $20 to make, but your copay is $60 because no rebate was negotiated. The price you pay isn’t based on the drug’s cost-it’s based on the contract behind the scenes.

Can my insurer change my drug’s tier mid-year?

Yes. About 17% of commercial plans changed their formularies between January and June 2023. Insurers can move drugs to higher tiers if the rebate deal expires or if a competitor offers a better one. You’ll usually get a notice in the mail, but many people miss it. Always check your formulary before refilling, especially if you’re on a chronic medication.

Are all generics the same?

In terms of active ingredients, yes. The FDA requires generics to be bioequivalent to the brand. But inactive ingredients (fillers, dyes, coatings) can vary. For most people, this doesn’t matter. But for a small number of patients-like those with severe allergies or absorption issues-switching generics can cause problems. That’s why your doctor should be consulted before any substitution.

What’s the difference between a preferred and non-preferred generic?

There’s no clinical difference. The terms “preferred” and “non-preferred” are purely financial. Preferred means the manufacturer gave the PBM a big discount. Non-preferred means they didn’t. Your plan encourages you to pick the preferred version by making it cheaper. But both versions work the same way.

Can I get help paying for a high-tier generic?

Yes. Many drug manufacturers offer patient assistance programs that cover part or all of the cost for eligible people. You can also use nonprofit organizations like the Patient Advocate Foundation or NeedyMeds. Some pharmacies offer discount cards through GoodRx that can slash your price below your copay. Always ask your pharmacist-many don’t bring it up unless you ask.

Laia Freeman January 29, 2026

This is insane!! I just got charged $60 for my generic lisinopril-same pill I’ve taken for 5 years!! My pharmacist said it’s ‘non-preferred’ now?? Like, what does that even mean?? I didn’t change anything!! Why am I paying more for the SAME THING?? This system is rigged!!

rajaneesh s rajan January 29, 2026

So let me get this straight: the pill doesn’t change, the doctor doesn’t change, but your wallet gets lighter because some suit in a cubicle got a better kickback? Welcome to capitalism, baby. At least we still have GoodRx. And also, the fact that we’re all here screaming into the void together? That’s the only real therapy left.

paul walker January 30, 2026

I had this happen with my diabetes med last month. I called my doc, asked for a therapeutic interchange, and they approved it in 2 days. Took me 10 minutes on the phone. Don’t let them scare you-ask. Always ask. Seriously. It works more than you think.

Alex Flores Gomez January 31, 2026

Look, if you can’t afford your meds, maybe you shouldn’t be taking them. This is why people need to stop expecting healthcare to be free. You think your $5 generic is ‘fair’? That’s because the PBM is subsidizing you with rebates from other patients. Wake up. The system isn’t broken-it’s optimized. You’re just not the priority.

Frank Declemij February 1, 2026

Formulary tiers are a well-documented cost-containment strategy used by PBMs to drive utilization toward lower-cost alternatives. The clinical equivalence of generics is mandated by the FDA, but commercial decisions are independent of therapeutic outcomes. Patients should always verify tier status before filling prescriptions, as formularies change quarterly.

Pawan Kumar February 2, 2026

It’s not just PBMs. It’s the entire pharmaceutical-industrial complex. The FDA? Complicit. The AMA? Silent. Your doctor? Paid by pharma reps. They want you dependent. They want you confused. They want you paying $2,000 for a generic that costs $3 to make. This is not an accident. This is a war on the poor.

DHARMAN CHELLANI February 3, 2026

Generic? More like generic-level scam. You think you’re saving money? You’re just funding the PBM’s yacht. Next thing you know, they’ll charge you extra for the pill bottle. Seriously. Who’s next? The air inside the bottle?

Keith Oliver February 3, 2026

Everyone’s acting like this is new. Newsflash: this has been going on since 2010. I’ve been tracking this since my first Tier 4 generic. You don’t get it? Fine. But if you think your doctor’s gonna fix it, you’re even more naive than I thought. Read the formulary. Every. Single. Time. Or stop complaining.

Andy Steenberge February 5, 2026

Hey, if you’re struggling with this, you’re not alone. I used to feel the same way until I started using NeedyMeds and GoodRx together. Sometimes the cash price is half your copay. And if your doctor won’t help, call your insurer’s patient advocate line-they’re actually helpful. You’ve got options. Don’t give up.

kabir das February 6, 2026

I cried last week when I saw my bill... I just wanted to take my meds... I didn’t ask for this... Why does it have to be so hard? I’m tired... So tired... I just want to live...

LOUIS YOUANES February 7, 2026

Let me tell you something about PBMs. They’re not even regulated like real companies. They’re private equity ghosts. They buy up pharmacies, then charge them to fill prescriptions. Then they charge you to get the drug. Then they charge the manufacturer to be on the formulary. It’s a pyramid. And you? You’re at the bottom. Paying for everyone’s profit.

Robin Keith February 9, 2026

Think about it: the entire healthcare system is built on the illusion of choice. We’re told we have options, but the only real option is who gets to profit from your illness. The PBM doesn’t care if you live or die-they care if the rebate check clears. The doctor doesn’t control the tier. The pharmacist doesn’t set the price. The manufacturer doesn’t decide where it lands. And you? You’re just a number in a spreadsheet that says ‘cost avoidance.’ We’ve turned medicine into a derivatives market. And we wonder why people stop taking their pills. Of course they do. Why would you trust a system that treats your health like a financial instrument?